Expectations surrounding functionality within mobile banking apps are higher than ever, as consumers engage more and more with mobile and tablet devices. Banks and credit unions are trying to balance consumer desire for simplicity while providing access to tools that were once the domain of desktops. Here are the best of what we see globally.

- Simplicity: The ability to remove steps or make a current process easier to perform

- Engagement: The ability to encourage greater user involvement that will increase loyalty

- Contextuality: The ability to leverage user insight to improve the functionality of an app

Mobile Banking Trends

In fact, many of the comments made by the dozens of participants in the discussion revolved around simplicity of design, the removal of friction and the ability to improve the customer experience. Mobile Banking Series: State of the Market 2014,’ an analysis of current mobile banking functionality found the following trends:

- Consumers expectations around mobile banking are higher than ever as use of mobile banking increases at the expense of desktop banking.

- 100% of the banks surveyed support both iPhone and Android devices, with 60% supporting Windows and fewer financial institutions investing in Blackberry support.

- 24% of banks surveyed allow balances to be viewed before login, 29% allow mobile blocking of a credit or debit card, and 68% allow the viewing of future transactions post login.

- 72% of banks allow a user to save their ID on the mobile app while only 26% require mobile specific login details.

- While the vast majority of banks integrate savings, overdraft and credit cards within the mobile banking app, far fewer include loans or investments.

- 91% of banks allow consumers to make payments to an existing payee, roughly half allow the payment to a new payee or mobile phone number, while only 14% allow payment to an email address and 2% using social media.

- Sales and marketing as well as the ability to buy products within the mobile banking app is available at fewer than 30% of the banks monitored.

- Secure messaging is available at 30% of the organizations, with live chat only provided by 7% of the institutions.

Overall, the Mapa Research report found that while many innovations have been introduced in the past 12 months, other mobile banking functionalities that were once considered ‘new’ are now simply table stakes in the competition to improve the consumer experience.

Enhanced Mobile Banking Engagement

From account opening to the login and home screen, financial institutions are working on new ways to create a simple and engaging first step for the mobile banking customer. As more institutions are providing easy ways to leverage the camera within a smartphone to facilitate account opening, others are providing more functionality prior to login (such as viewing balances) and are redesigning their home pages to generate greater engagement using icons, personalization options and visuals.

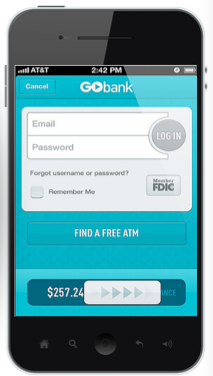

GoBank pre-login balance inquiry

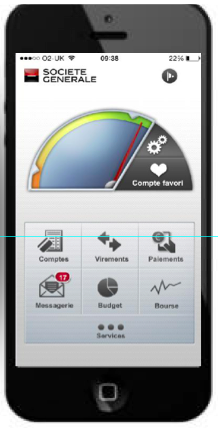

Societe Generale visual balance and icon login

Barclays mobile app with personalization option

BNP Paribas allows customers to have multiple mobile users on one device

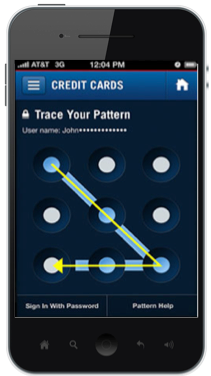

Capital One eliminates forgotten passwords with Sure Swipe

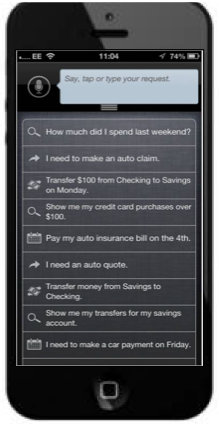

USAA provides members hands-free voice command capability

LaCaixa has moved to icon-based login screen

Improved Mobile Banking Payment Functionality

One of the key drivers of increased usage of mobile banking apps is the ability for customers to do more within the app. Greater self-servicing capability, payment functionality and account integration are all moving from the desktop to the mobile device. As functionality increases, so does the challenge of maintaining a good user experience as the mobile applications begin to feel busy. In the past year, banks seem to have focused primarily on adding functionality, but future spoils will go to those who are able to combine increased functionality with an improved user experience through better navigation and design.

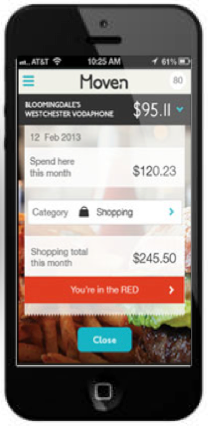

Moven provides instant digital receipts

Kaching provides several one-touch payment options

Barclays provides integrated borrowing calculator within mobile app

Bank of America provides mobile billpay payee additions

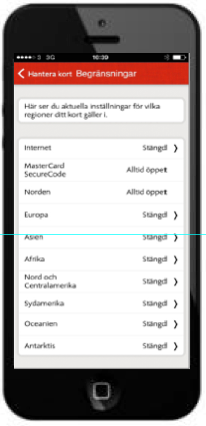

ICA Banken allows customers to select regions where cards can be used

Expanded Mobile-First Capabilities

Using the GPS and photo capabilities inherent within a smartphone, many banks are now providing unique capabilities that enhance the customer experience and provide potential revenue opportunities for financial institutions. These are apps that many believe are the future of mobile banking because of the ease of use and digital value provided. A small number of banks have been introducing digital storage where consumers can store important information, usually pertaining to accounts held at the bank, but sometimes expanding to insurance documents, etc. Barclays is one of the first provider to introduce Cloud Storage. The usefulness and logistics of digital storage is still being evaluated by many banks and credit unions.

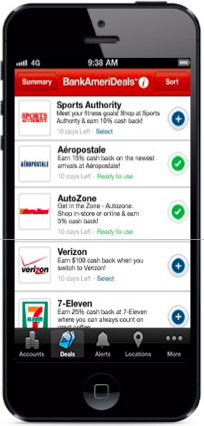

Bank AmeriDeals can leverage location to pinpoint reward offers

Augmented reality is used for new home finder app at Halifax in the UK

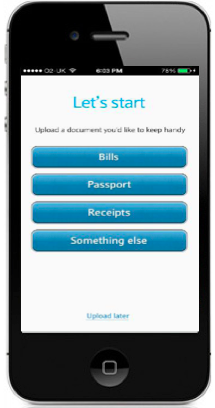

Barclays provides a digital lockbox for important documents

Customers of Natwest can make cardless withdrawals at ATMs

Improved Sales and Service

Despite all of the improvements to mobile banking over the past couple of years, mobile sales and service has lagged. This is the key to a true omnichannel experience, however, as financial institutions hope to migrate more costly transactions from the branch or call center to more of a self-service mode. Calculators and comparison tools have been introduced in the past 9 months, but sales and monetization in the app are still not common. It is believed that part of the reason for lack sales integration is related to the challenge of selling within a limited space and at the same time not being too intrusive or disturbing to the consumer. One functionality with great growth potential is allowing the consumer greater access to customer support from the secure site either via live chat or a secure click to call. At this point, most mobile customer service is done through text messaging.

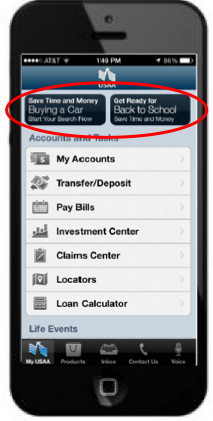

USAA is one of only a few banks that integrate sales messages within the mobile app

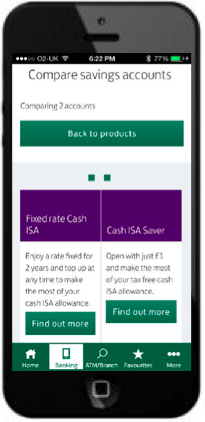

Lloyds provides product comparison charts within mobile app

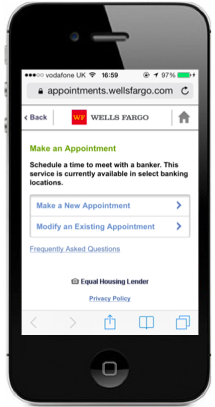

Wells Fargo allows customers to set appointments using their mobile device

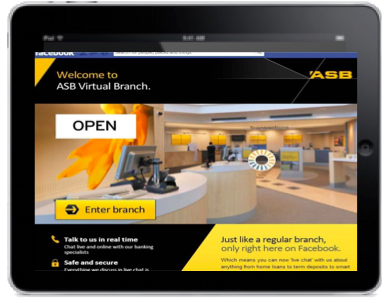

ASB has developed a virtual branch to field inquiries from customers

No comments:

Post a Comment