developereconomics.com

In 2003 Europe’s mobile operators launched Simpay, promising to let us buy flowers and concert tickets across Europe, with the price added to our mobile phone bill. By 2005 that had morphed into PayForIt, for UK operators only but with similar aspirations, and a similar lack of success. A decade later, mobile network operators are still being cut out of the payment loop, but not for lack of trying.

Operator billing should be the perfect m-commerce platform: Mobile operators store prepaid credit for 77% of their customers, according to the GSMA, and have credit agreements with the other 23%. They have experience dealing with critical systems, and real-time credit checking systems built to take huge loading, so they should be the obvious winners in the m-commerce business. As then-CEO of Vodafone Arun Sarin told the FT in 2007:

“The simple fact that we have the customer and billing relationship is a hugely powerful thing that nobody can take away from us … Whoever comes into the marketplace is going to have to work through us.”

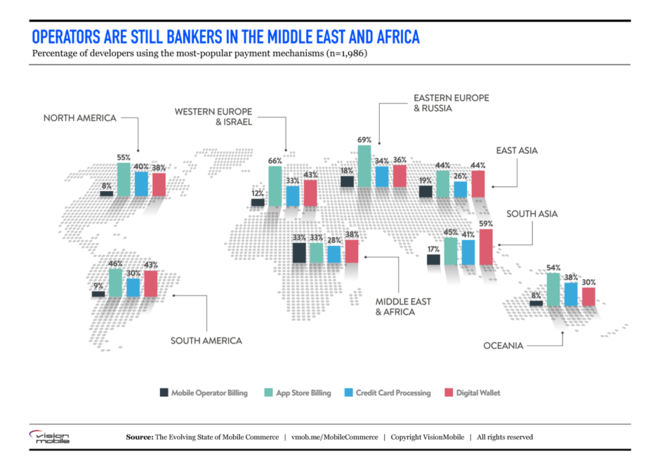

Only they didn’t, and they don’t, and these days operator billing is a minority pastime everywhere – except Africa and the Middle East.

The data comes from the VisionMobile Developer Economics survey, which reached more than 11,000 mobile developers at the start of 2016. Almost 2,000 of those developers are involved in m-commerce, but only 16% of those have integrated operator billing into their applications.

In Europe, where operators have perhaps tried the hardest to become the wallet of the future, that number drops to 12%, and in North America only 8% of m-commerce developers have bothered to work with the operator to handle billing. In 2010 Verizon launched its own payment service, based on the BilltoMobile platform, but BilltoMobile has been losing money ever since, and in May this year was purchased by UK payment processor Bango.

The argument against operator billing has always been that of interoperability – developers integrating with one mobile operator’s billing system would have to port their code to support another. That was the problem that Simpay, and PayforIt, were designed to solve, and they are far from alone in solving that.

The GSMA’a OneAPI started out as platform for interfacing with SMS Centres and network call management, but quickly focused into a cross-operator billing system to attract operators who proved reluctant to spend money implementing the whole standard. Even GSMA’s decision to host a OneAPI proxy (making it much easier for operators to integrate) wasn’t enough for the operators, and the standard now languishes as a vertical API within a handful of network operators.

In May 2016 yet another attempt was made, with nine of the largest mobile operators joining up to endorse the “Open API” from the TM Forum (an industry body with a decent history of setting architectural standards in infrastructure). This latest set of APIs covers a very wide remit, but includes much that the OneAPI set out to achieve including the resolution of billing events.

Other cross-operator alternatives, such as Telefónica’s BlueVia, have achieved some level of success, but it is probably too late for mobile operators to become the default billing platform they imagined that they would be. Only in the Middle East and Africa is mobile operator billing being used by a significant proportion of m-commerce developers; everywhere else that role is being filled by other players.

Just as Apple and Google provided operator-independent app stores, those companies provide the perfect alternative for developers looking to collect money. Billing through the app store itself, or via the electronic wallets run by Apple and Google, is increasingly popular – and both companies have extended the functionality in recent months.

Credit cards also remain popular. Most credit card processing is done via third-party companies, such as Braintree and Stripe, who compete to provide the best APIs and value-added services. Meanwhile various banking consortia are jumping into the frame, and Visa and MasterCard are funding various competitions intended to raise the profile of their own developer programs, and demonstrate their utility beyond basic transaction processing.

With such strong competition in place the opportunity for operators to step in and take the market is long gone, and developers won’t be easily wooed away from third-party providers. With a coordinated approach the operators certainly could have grabbed the market, but arrogance, lethargy – and the fear of creating an illegal cartel – prevented that future from happening.

The world of mobile commerce is evolving fast, and is only going to become more important as it grows and changes so rapidly, but mobile network operators will struggle to be more than a big player in it.

If you’d like to know more about which m-commerce platforms are gaining ground, or what developers are looking for in an m-commerce platform, then take a look at The evolving state of mobile commerce, a report published by VisionMobile in collaboration with Braintree.

In 2003 Europe’s mobile operators launched Simpay, promising to let us buy flowers and concert tickets across Europe, with the price added to our mobile phone bill. By 2005 that had morphed into PayForIt, for UK operators only but with similar aspirations, and a similar lack of success. A decade later, mobile network operators are still being cut out of the payment loop, but not for lack of trying.

Operator billing should be the perfect m-commerce platform: Mobile operators store prepaid credit for 77% of their customers, according to the GSMA, and have credit agreements with the other 23%. They have experience dealing with critical systems, and real-time credit checking systems built to take huge loading, so they should be the obvious winners in the m-commerce business. As then-CEO of Vodafone Arun Sarin told the FT in 2007:

“The simple fact that we have the customer and billing relationship is a hugely powerful thing that nobody can take away from us … Whoever comes into the marketplace is going to have to work through us.”

Only they didn’t, and they don’t, and these days operator billing is a minority pastime everywhere – except Africa and the Middle East.

The data comes from the VisionMobile Developer Economics survey, which reached more than 11,000 mobile developers at the start of 2016. Almost 2,000 of those developers are involved in m-commerce, but only 16% of those have integrated operator billing into their applications.

In Europe, where operators have perhaps tried the hardest to become the wallet of the future, that number drops to 12%, and in North America only 8% of m-commerce developers have bothered to work with the operator to handle billing. In 2010 Verizon launched its own payment service, based on the BilltoMobile platform, but BilltoMobile has been losing money ever since, and in May this year was purchased by UK payment processor Bango.

The argument against operator billing has always been that of interoperability – developers integrating with one mobile operator’s billing system would have to port their code to support another. That was the problem that Simpay, and PayforIt, were designed to solve, and they are far from alone in solving that.

The GSMA’a OneAPI started out as platform for interfacing with SMS Centres and network call management, but quickly focused into a cross-operator billing system to attract operators who proved reluctant to spend money implementing the whole standard. Even GSMA’s decision to host a OneAPI proxy (making it much easier for operators to integrate) wasn’t enough for the operators, and the standard now languishes as a vertical API within a handful of network operators.

In May 2016 yet another attempt was made, with nine of the largest mobile operators joining up to endorse the “Open API” from the TM Forum (an industry body with a decent history of setting architectural standards in infrastructure). This latest set of APIs covers a very wide remit, but includes much that the OneAPI set out to achieve including the resolution of billing events.

Other cross-operator alternatives, such as Telefónica’s BlueVia, have achieved some level of success, but it is probably too late for mobile operators to become the default billing platform they imagined that they would be. Only in the Middle East and Africa is mobile operator billing being used by a significant proportion of m-commerce developers; everywhere else that role is being filled by other players.

Just as Apple and Google provided operator-independent app stores, those companies provide the perfect alternative for developers looking to collect money. Billing through the app store itself, or via the electronic wallets run by Apple and Google, is increasingly popular – and both companies have extended the functionality in recent months.

Credit cards also remain popular. Most credit card processing is done via third-party companies, such as Braintree and Stripe, who compete to provide the best APIs and value-added services. Meanwhile various banking consortia are jumping into the frame, and Visa and MasterCard are funding various competitions intended to raise the profile of their own developer programs, and demonstrate their utility beyond basic transaction processing.

With such strong competition in place the opportunity for operators to step in and take the market is long gone, and developers won’t be easily wooed away from third-party providers. With a coordinated approach the operators certainly could have grabbed the market, but arrogance, lethargy – and the fear of creating an illegal cartel – prevented that future from happening.

The world of mobile commerce is evolving fast, and is only going to become more important as it grows and changes so rapidly, but mobile network operators will struggle to be more than a big player in it.

If you’d like to know more about which m-commerce platforms are gaining ground, or what developers are looking for in an m-commerce platform, then take a look at The evolving state of mobile commerce, a report published by VisionMobile in collaboration with Braintree.

No comments:

Post a Comment